Vanguard Australia posted this interview to their website at the beginning of the month. The content and clarity of the article make it a good read.

Vanguard | 01 August 2013

As global equity markets continue to heat up, we sat down with Angus McLeod, Portfolio Manager in Vanguard’s Equity Investment Group to ask him some questions currently facing equity investors – from market valuations and currency hedging decisions to the impact of China’s slowdown on our domestic market.

The US and UK equity markets are close to all-time highs, while the Australian market is trading significantly lower. Why is that the case when our economy is stronger?

World markets reached a pre-GFC high point in mid-2007, then over the next six months fell between 40 per cent and 60 per cent and have since staged a strong recovery. The US equity market has been the best performer since the GFC and is up around 140 per cent, the UK has recovered 86 per cent, the pan-European index is up 68 per cent but the Australian index has lagged, rising only 61 per cent from its low point. There are two main explanations for the underperformance of the Australian market during this time: US monetary policy and Australia’s reliance on China.

US authorities pulled out all stops to save the American economy. A combination of zero interest rates and massive intervention from the Federal Reserve to print money and to purchase debt flooded the system with liquidity.

As these policies started to produce results the US equity market (which is a leading indicator of the economy) surged. Europe, despite deep-seated problems in its peripheral economies, also recovered. A rising tide lifts all boats but the Australian economy is tethered to the performance of the Chinese economy which, in the recent past, has slowed from its 15 per cent pa GDP growth to a modest 7.5 per cent. Thus the outlook for Australia is more subdued, even though our GDP growth rate has outpaced most of the developed world since 2007.

Australia was seen as a safe haven while China’s growth spurt continued. The local currency stayed well above parity with the US dollar and the stock indices rose. Resources investment flooded in, our strong financial sector attracted yield investors and the economy enjoyed what has turned out to be a 20 year boom.

In recent months the growth drivers of the domestic economy have changed: the mining investment cycle has matured, the outlook for the Chinese economy and the structural changes being investigated there are set to turn the economy away from manufacturing exports towards domestic consumption.

On top of that, the US economic recovery is gaining traction. In May this year market speculation that central bank support for the US economy would be withdrawn saw a major realignment of investment market allocations. Safe haven market investments were rotated to domestic US investments which, for Australia, saw the equity market sold down 10 per cent (it’s since recovered to be down 5 per cent) and the domestic currency to tumble from 1.03 to the low 0.90s against the greenback. All indications from the US Fed are that accommodative monetary policy will continue as long as is required to maintain momentum in the economic recovery there. This is generally positive for US equities. As China’s domestic economy loses momentum – even while still growing at 7.5 per cent – the outlook for commodity-based exporters such as Australia is relatively less optimistic. Since stock markets tend to anticipate developments in the real economy the differential outlook for equities markets is the best explanation for Australia’s relative underperformance.

The International Monetary Fund (IMF) has recently revised down China’s GDP. What effect will this have on the Australian economy and market given that China is our largest trading partner?

From almost zero in the early 1990s, Australia’s bilateral trade with China is now valued at over $120 billion annually, about 20 per cent of all trade. China takes almost a third of goods exports and is the destination for nearly a quarter of our coal and a fifth of our iron ore exports. As such, the Australian economy is highly exposed to the Chinese economy, particularly its manufacturing sector which is the main user of Australia’s commodity raw materials.

That said, and even though the IMF has lowered its outlook for Chinese growth, government authorities are mindful that the stability of the domestic Chinese economy should be maintained. They’re also well aware of their economy’s potential to affect global growth. Premier Li, speaking in July this year, reiterated that the bottom of a reasonable range of GDP growth was 7 per cent. As one of few economies with centralised control, the ability of China to direct restructuring and development as needed is a valuable tool.

Australia’s worst-case outcome is a hard-landing of the Chinese economy where growth falls dramatically. While unlikely, such a move poses significant downside risks to the Australian share market, where resources and energy companies make up 20 per cent of capitalisation. China’s appetite for Australian iron ore saw the spot price rise to over USD180 per tonne at the height of the resources boom but as demand has fallen the price has declined to USD118. As the iron ore state, Western Australia has been most affected: 23 per cent of gross state product is made up of exports to China. Should a hard landing eventuate, the exchange rate may continue to weaken, absorbing some of the growth shock, and federal deficits would expand while the RBA would be forced to cut interest rates to promote domestic demand. Some analysts suggest this hard-landing scenario could cut Australian growth by 1.4 percentage points; clearly it’s a situation we’d be keen to avoid.

The Australian economy is exposed to the fortunes of China and vulnerable to economic developments there. Chinese authorities’ control of the economy is strong but their capacity to keep the growth engine ticking over at above 7 per cent is critical to Australia’s economic outlook.

We have seen the Australian dollar depreciate against the US dollar of late. Should I hedge or unhedge my international portfolios?

The Australian dollar has fallen around 13 per cent against the greenback since the start of May, mostly due to the threat of the withdrawal of quantitative easing by US authorities and the emergence of data showing that the US economy’s recovery is self-sustaining. The question for an Australian investor in international equities as to whether or not to hedge currency exposure appears perplexing at first, but a closer analysis of currency markets reveals a simpler answer. Unlike investors in the US, Europe and the UK domestic Australian investors’ portfolios are based in a currency which is positively correlated to global risk. As investor appetite for what’s commonly called the “risk on” trade is high the Australian dollar tends to rise and when the “risk off” trade prevails the AUD tends to fall. Thus an Australian investor in international equities tends to have a natural hedge against currency movements which assists in smoothing out the volatility of returns.

Some investors may, understandably, find that currency volatility is too much to bear. As a compromise between currency diversification benefits and the added volatility from foreign exchange exposure, many investors choose a 50 per cent hedge over the long term. This acknowledges the difficulty of correctly predicting currency movements.

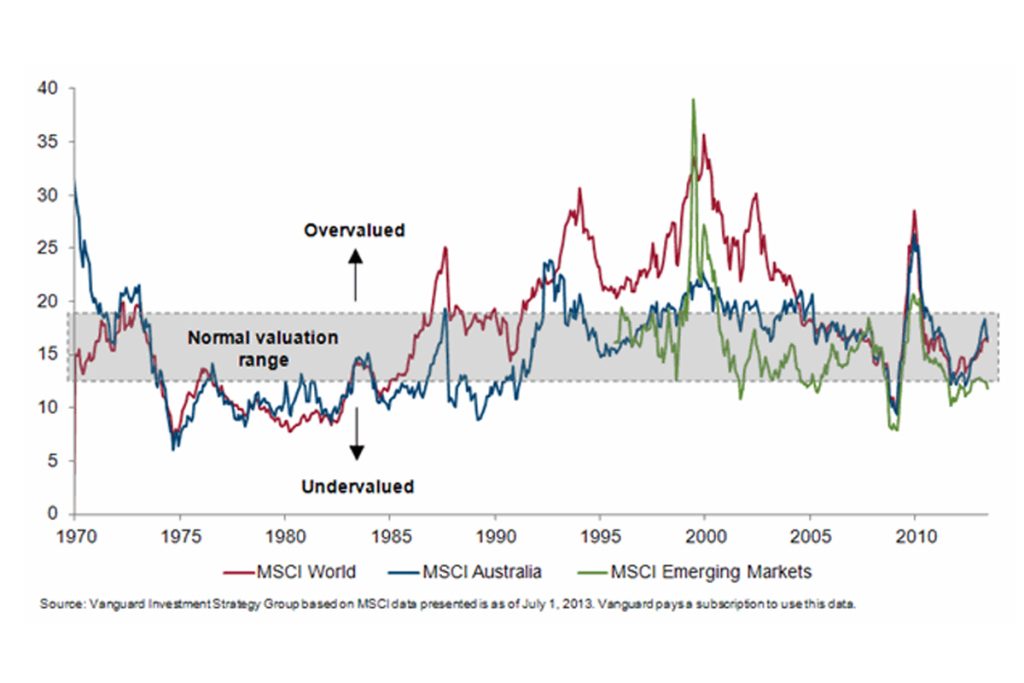

There are currently concerns that global share markets may have overheated as a result of monetary stimulus (quantitative easing). What is Vanguard’s view on equity valuations at the moment? Are price-to-earnings ratios currently in the high, low or normal range?

It’s fair to say that monetary stimulus in the UK, Europe, Australia, Japan and most notably the US has been responsible for the sustained strength of global share markets in the aftermath of the GFC. In fact, recent falls in stock indices have occurred as speculation as to its near-term withdrawal has frightened fast money equity participants. Equity markets tend to foreshadow the real economy and there is a danger that share market valuations, as measured by price to earnings ratios, can get a little ahead of themselves. Shown in the chart below, our recent analysis of global valuations shows that, at current levels, global equity markets are within the normal valuation range for world developed market equities and Australian equities.

Historical price to earnings ratios

What is Vanguard’s outlook on equity markets at the moment?

Vanguard believes that a well-diversified portfolio of investments should always contain an allocation to equities through all market cycles and economic conditions. While equities are a more volatile asset class, over the long-term investors are generally rewarded by receiving the extra return that goes along with accepting additional risk. Equities are a valuable source of investment growth. Returns include income from dividends as well as capital appreciation.

Vanguard’s Capital Markets Model®, which examines a broad range of investment classes and analyses various portfolio combination scenarios, suggests that the return on equities will be broadly in line with historical averages at around 9.9 per cent. Global inflation expectations are well below historical averages so investors get to “keep” more of their nominal returns rather than losing out to inflation. In the medium term, our model indicates a positive outlook for equities, despite expectations for subdued economic growth overall.

Share market investors should always bear in mind that a consistent approach to equities, unperturbed by market gyrations, is an important part of capturing the equity return premium. Growth potential and diversification aside, an equity allocation is an important part of an investment portfolio.

GENERAL ADVICE WARNING

Vanguard Investments Australia Ltd (ABN 72 072 881 086 / AFS Licence 227263) is the product issuer. We have not taken yours and your clients’ circumstances into account when preparing our website content so it may not be applicable to the particular situation you are considering. You should consider yours and your clients’ circumstances and our Product Disclosure Statement (PDS) or Prospectus before making any investment decision. You can access our PDS or Prospectus online or by calling us. This website was prepared in good faith and we accept no liability for any errors or omissions. Past performance is not an indication of future performance.